Top 10 Food Safety Testing and Technologies Trends (Food Safety, GM Food Safety, Food Pathogen, Meat Speciation, Food Authenticity, Pesticide Residue, Mycotoxin, Allergen, Water, and Bottled Water) - Global Forecast to 2022

Top 10 companies in Top 10 Food Safety Testing and Technologies Trends

[335 Pages Report] The food safety testing and technologies market is projected to reach USD 39.47 Billion by 2022. It encompasses a variety of testing technologies market, among them the meat speciation testing market is projected to reach a value of USD 2.22 Billion by 2022, at the highest CAGR of 8.2% from 2016 to 2022, and bottled water testing equipment market is projected to reach a value of USD 6.80 Billion by 2022, at a CAGR of 5.3% from 2016 to 2022. The base year considered for the study is 2015, and the forecast period is from 2016 to 2022. The basic objective of the report is to understand the market by identifying various subsegments in the food safety testing and technologies market.

The other objectives include:

- To analyze emerging trends and opportunities in the global food safety testing and technologies market

- To study the global market with focus on high-growth applications in each vertical and the fastest-growing markets

- To provide detailed information about crucial factors influencing the growth of the market (drivers, restraints, opportunities, and challenges)

- To strategically analyze micromarkets with respect to individual growth trends, future prospects and their contribution to the total market

- To analyze opportunities in the market for stakeholders and provide details of the competitive landscape for market leaders

- To forecast the size of the global food safety testing and technologies market and its various submarkets with respect to four main regions, namely, North America, Asia-Pacific, Europe, and Rest of the World (RoW)

- To strategically profile key players and comprehensively analyze their core competencies

- To analyze competitive developments such as new service launches, acquisitions, expansions, investments, partnerships, agreements, joint ventures, and collaborations in the food safety testing market

This report includes estimations of the top 10 trends in the food safety testing and technologies industry in terms of value (USD million). Both top-down and bottom-up approaches have been used to estimate and validate the size of the global food safety testing and technologies market and to estimate the size of various other dependent submarkets in the overall market. The key players in the market have been identified through secondary research, some of the sources are press releases, paid databases such as Factiva and Bloomberg, annual reports, and financial journals; their market share in respective regions has also been determined through primary and secondary research. All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

To know about the assumptions considered for the study, download the pdf brochure

Key participants in the supply chain of the food safety testing and technologies market are the product manufacturers, end use industries, food and water safety policy regulators, and raw material suppliers. The key players that are profiled in the report include SGS S.A. (Switzerland), Bureau Veritas S.A. (France), Intertek Group plc (U.K.), Eurofins Scientific SE (Luxembourg), ALS Limited (Australia), Thermo Fisher Scientific Inc. (U.S.), Mérieux NutriSciences Corporation (U.S.), AsureQuality Ltd. (New Zealand), Microbac Laboratories Inc. (U.S.), and Romer Labs Diagnostic GmbH (Austria).

This report is targeted at the existing players in the industry, which include the following:

- Food processors and manufacturers

- R&D institutes & technology providers

- Wastewater treatment plants

- Water pumping plants

- Reagent manufacturers and suppliers

- Diagnostic instrument and kit manufacturers/suppliers of environmental testing

- Bottled water testing equipment manufacturers/suppliers

- Government authorities

“The study answers several questions for stakeholders, primarily which market segments to focus on in next two to five years for prioritizing efforts and investments.”

Get online access to the report on the World's First Market Intelligence Cloud

Request Sample Scope of the Report

The food safety testing and Technologies industry has been segmented into:

-

Food safety testing market

- Food safety testing market

- GM food safety testing market

- Food pathogen testing market

- Meat speciation testing market

- Food authenticity testing market

- Pesticide residue testing market

- Mycotoxin testing market

- Allergen testing market

-

Water safety testing & technologies market

- Water testing and analysis market

- Bottled water testing equipment market

On the basis of Region, the food safety testing and technologies industry has been segmented into:

- North America

- Europe

- Asia-Pacific

- RoW

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the company’s specific needs.

The following customization options are available for the report:

Regional Analysis

- Further country-specific data and its market analysis

Company Information

- Detailed analysis and profiling of additional market players (up to five)

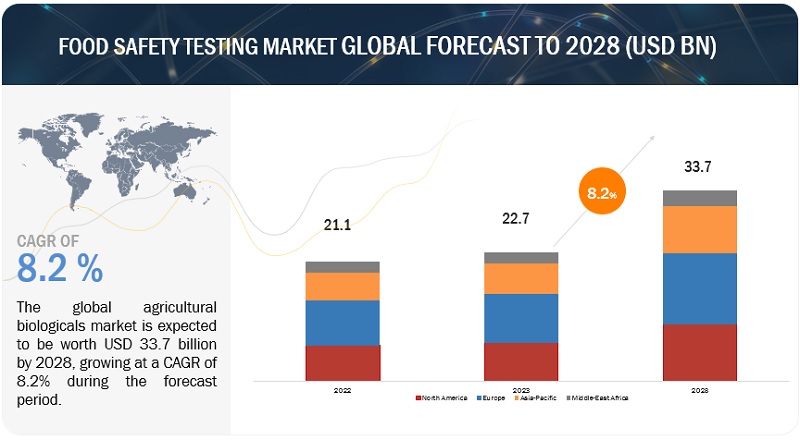

The top 10 Food safety testing and technologies market is projected to reach USD 39.47 Billion by 2022. The Top 10 food safety testing and technologies industry includes food safety testing market, GM food safety testing market, food pathogen testing market, meat speciation testing market, food authenticity testing market, pesticide residue testing market, mycotoxin testing market, and allergen testing market. The markets covered under water safety testing & technologies include water testing and analysis and bottled water testing.

The growth of the food safety testing market is estimated to be high in most regions. Increase in foodborne illness outbreaks, implementation of stringent food safety regulations globalization of food supply, and availability of advanced technology capable of rapid testing are the major driving factors of this market. On the other hand, lack of food control infrastructure & resources in developing countries, and lack of awareness about safety regulations among food manufacturers are major hindrances for the growth of the market, globally. Change in lifestyles, increase in demand for convenience foods, and increase in food trade and export and import across borders in emerging markets have been key opportunities for the food safety testing market.

The global market for GM food safety testing is projected to exhibit a strong growth due to the current food shortage that the world is experiencing. Ensuring proper food and nutrient supply is the most important driver which is influencing the GM food safety testing market. GM food safety testing market is also rising due to the continuously evolving technologies used in agriculture that has resulted in a shift in farming practices. Growth in investment in the research and development of genetically modified products is another driver leading the market.

The water safety testing & analysis market is projected to grow at a rapid pace due to stringent hygiene standards, mandatory need for pure drinking and utility water, and increase in government and private funding for tackling environmental issues. All government and private sectors across the globe are stressing on the innovation process for increasing the efficiency of water safety testing and providing incentives, financial support, advisory services, and facilities for water testing and analysis to improve and maintain the water quality for human consumption.

The major restraining factors that affect the top 10 trends in the food safety testing and technologies industry are lack of food control infrastructure & resources in developing countries and lack of awareness about safety regulations among food manufacturers. Thus, companies must be proactive and carry out food safety testing to avoid contamination. As food contamination is most likely to take place in the supply chain from production to consumption, risks can be identified by inspecting the backward flow of the supply chain.

SGS S.A. (Switzerland), Bureau Veritas S.A. (France), and Intertek Group plc (U.K.) are some of the prominent players in the top 10 trends in food safety testing and technologies industry; these companies focused on expanding their product manufacturing capacities, to cater to the large customer base to develop new products.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Table of Contents

1 Introduction (Page No. - 34)

1.1 Objectives of the Study

1.2 Market Definitions

1.3 Periodization

1.4 Currency

1.5 Stakeholders

2 Research Methodology (Page No. - 38)

2.1 Research Data

2.1.1 Secondary Data

2.1.1.1 Key Data From Secondary Sources

2.1.2 Primary Data

2.1.2.1 Key Data From Primary Sources

2.2 Factor Analysis

2.2.1 Introduction

2.2.2 Demand-Side Analysis

2.2.2.1 Worldwide Increase in Outbreak of Foodborne Illnesses

2.2.2.2 Rising Population

2.2.2.2.1 Increase in Middle-Class Population, 2009–2030

2.2.2.3 Developing Economies and Increasing GDP

2.2.2.4 Rise in the Number of Technical Barriers to Trade (TBT) Concerns Raised By the Wto

2.2.2.5 Globalization in Food Trade

2.2.3 Supply-Side Analysis

2.2.3.1 Growing Market for Food Diagnostics

2.2.3.2 Ease of Food Pathogen Testing and Reduction of Cost in Auditing Have Led to the Growth of Outsourced Food Pathogen Testing

2.3 Market Size Estimation

2.4 Market Breakdown & Data Triangulation

2.5 Research Assumptions & Limitations

2.5.1 Assumptions

2.5.2 Limitations

3 Executive Summary (Page No. - 52)

4 Premium Insights (Page No. - 59)

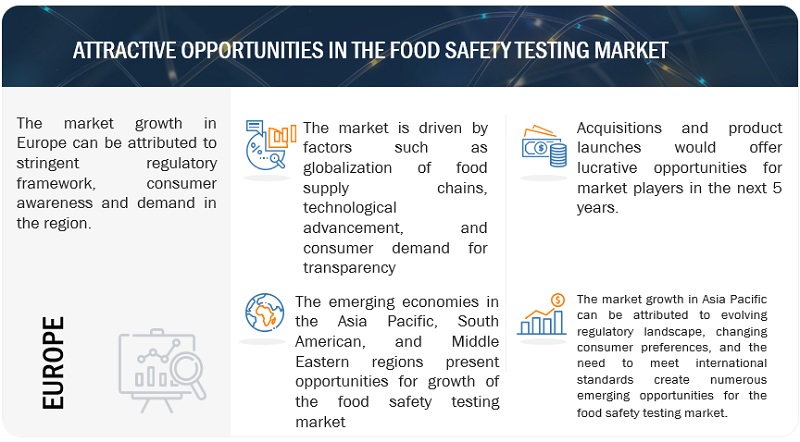

4.1 Opportunities in Food Safety Testing Market

4.2 Food Safety Testing Market: Major Countries

5 Food Safety Testing (Page No. - 61)

5.1 Market Definition

5.2 Market Overview

5.2.1 Introduction

5.2.2 Market Dynamics

5.2.2.1 Drivers

5.2.2.1.1 Worldwide Increase in Foodborne Illness Outbreaks

5.2.2.1.2 Implementation of Stringent Food Safety Regulations

5.2.2.1.3 Globalization of Food Supply

5.2.2.1.4 Availability of Advanced Technology Capable of Rapid Testing

5.2.2.1.5 Media Influence on Consumer Awareness About Food Safety

5.2.2.2 Restraints

5.2.2.2.1 Lack of Food Control Infrastructure & Resources in Developing Countries

5.2.2.2.2 Lack of Awareness About Safety Regulations Among Food Manufacturers

5.2.2.3 Opportunities

5.2.2.3.1 Emerging Markets for Food Safety Testing

5.2.2.3.2 Increasing Consumer Awareness About Food Safety

5.2.2.4 Challenges

5.2.2.4.1 Time-Consuming Testing Methods

5.2.2.4.2 Inappropriate Sample Collection Standardization

5.2.2.4.3 Lack of Harmonization of Food Safety Regulations

5.3 Competitive Landscape

5.3.1 Overview

5.3.2 Competitive Situations & Trends

5.3.2.1 Mergers & Acquisitions

5.3.2.2 Expansions

5.3.2.3 Joint Ventures, Agreements, Partnerships, Collaborations, & Accreditations

5.3.2.4 New Service & Technology Launches

5.4 Market Analysis

5.4.1 Regional Analysis

5.4.2 Food Safety Testing Market, By Contaminant

5.4.3 Food Safety Testing Market, By Technology

5.4.4 Food Safety Testing Market, By Food Tested

6 GM Food Safety Testing (Page No. - 84)

6.1 Market Definition

6.2 Market Dynamics

6.2.1 Introduction

6.2.1.1 Drivers

6.2.1.1.1 Need to Ensure Sufficient Nutrient Consumption

6.2.1.1.2 Technological Evolution of Farming Practices

6.2.1.1.3 Diverse Processed GM Foods Manufacturing

6.2.1.1.4 Labeling Mandates in Several Countries

6.2.1.1.5 High Investment in Biotech R&D

6.2.1.2 Restraints

6.2.1.2.1 Lack of Implementation of Regulations

6.2.1.2.2 Lack of Required Technical Know-How Among Farmers

6.2.1.3 Opportunities

6.2.1.3.1 Emerging Markets for GM Food Safety Testing

6.2.1.3.2 Increased Consumer Awareness About GM Foods

6.2.1.4 Challenges

6.2.1.4.1 Ban on Production of GM Crops

6.2.1.4.2 Unaffordability of Tests By Manufacturers

6.2.1.4.3 Inappropriate Sample Collection Standards

6.3 Competitive Landscape

6.3.1 Overview

6.3.2 Competitive Situation & Trends

6.3.2.1 Expansions & Investments

6.3.2.2 Acquisitions

6.3.2.3 New Product, Service, and Technology Launches

6.3.2.4 Agreements, Collaborations, and Partnerships

6.4 Market Analysis

6.4.1 Regional Market Analysis

6.4.2 GM Food Testing Market Analysis, By Trait

6.4.3 GM Food Testing Market Analysis, By Technology

6.4.4 GM Food Testing Market Analysis, By Crop & Processed Food Tested

7 Food Authenticity Testing (Page No. - 101)

7.1 Market Definition

7.2 Market Overview

7.2.1 Introduction

7.2.1.1 High Investment and R&D Trend in Biotech & Food Authenticity Testing Technologies

7.2.2 Market Dynamics

7.2.2.1 Drivers

7.2.2.1.1 Implementation of Stringent Regulations in Developed Countries

7.2.2.1.2 Increasing Incidences of False Labeling & Certification

7.2.2.1.3 Increased EMA (Economically Motivated Adulterations) Due to High Competition

7.2.2.1.3.1 Addition of Exogenous Substance

7.2.2.1.3.2 Addition of Endogenous Substance

7.2.2.1.4 Increase in Incidence of Food Frauds

7.2.2.1.4.1 Usage of Banned Ingredients

7.2.2.1.4.2 Products Originating From Banned Processes Or Banned Geographic Areas

7.2.2.1.4.3 Consumer Complaints & Food Recalls

7.2.2.1.5 Growing International Trade

7.2.2.1.5.1 Complexity of Supply Chain

7.2.2.1.5.2 Cross Contamination Due to Complex Processes

7.2.2.1.6 Growing Awareness Among Consumers About Food Authenticity and Regulations

7.2.2.2 Restraints

7.2.2.2.1 Lack of Food Control Infrastructure & Resources in Developing Countries

7.2.2.2.2 Complexity in Testing Techniques

7.2.2.2.2.1 Difficulties in Detection of Unknown Adulterants By Chemical Tests

7.2.2.2.2.2 Varying Test Results With Test Methods

7.2.2.2.3 Lack of Harmonization of Regulations

7.2.2.3 Opportunities

7.2.2.3.1 Emerging Markets in Asian, African, and Other Countries.

7.2.2.3.2 Technological Advancements in the Industry & Test Kits for Onsite Testing

7.2.2.4 Challenges

7.2.2.4.1 Unaffordability of Tests By Manufacturers

7.2.2.4.2 Inappropriate Sample Collection & Standardization

7.3 Competitive Landscape

7.3.1 Overview

7.3.1.1 Key Market Strategies

7.3.1.2 Competitive Situation and Trends

7.3.1.2.1 Expansions & Investments

7.3.1.2.2 Acquisitions

7.3.1.2.3 Agreements, Collaborations, Partnerships & New Technology Launches

7.3.1.2.4 New Service Launches

7.4 Market Analysis

7.4.1 Regional Market Analysis

7.4.2 Food Authenticity Testing Market Analysis, By Target Testing

7.4.3 Food Authenticity Testing Market Analysis, By Technology

8 Food Pathogen Testing (Page No. - 129)

8.1 Market Definition

8.2 Market Dynamics

8.2.1 Introduction

8.2.1.1 Drivers

8.2.1.1.1 Worldwide Increase in Outbreak of Foodborne Illnesses

8.2.1.1.2 Implementation of Stringent Food Safety Regulations

8.2.1.1.3 Availability of Advanced Technology Capable of Rapid Testing

8.2.1.1.4 Media Influence on Consumer Awareness for Food Safety

8.2.1.2 Restraints

8.2.1.2.1 Lack of Food Control Systems, Technology, Infrastructure & Resources in Developing Countries

8.2.1.3 Opportunities

8.2.1.3.1 Emerging Market Such as China & India to Attract Global Attention for Food Pathogen Testing

8.2.1.3.2 Increasing Consumer Awareness for Food Safety

8.2.1.4 Challenges

8.2.1.4.1 Inappropriate Sample Collection Standardization

8.2.1.4.2 Time Engaged in Food Trade to Encourage Growth of Pathogens

8.3 Competitive Landscape

8.3.1 Overview

8.3.2 Competitive Situation & Trends

8.3.2.1 Acquisitions

8.3.2.2 Expansions & Investments

8.3.2.3 Agreements, Collaborations, & Partnerships

8.3.2.4 New Service & Technology Launches

8.4 Market Analysis

8.4.1 Regional Market Analysis

8.4.2 Food Pathogen Testing Market Analysis, By Pathogen Type

8.4.3 Food Pathogen Testing Market Analysis, By Food Type

8.4.4 Food Pathogen Testing Market Analysis, By Technology

9 Meat Speciation Testing (Page No. - 151)

9.1 Market Definition

9.2 Market Overview

9.2.1 Introduction

9.2.2 Market Dynamics

9.2.2.1 Drivers

9.2.2.1.1 Increasing Number of Adulteration and Food Fraud Cases

9.2.2.1.2 Religious Beliefs Drive Demand for Speciation Testing

9.2.2.1.3 Compliance With Labeling Laws

9.2.2.1.4 Stringent Regulation and Consumer Demand for Certified Products

9.2.2.2 Restraints

9.2.2.2.1 Lack of Food Control Systems, Technology, Infrastructure, and Resources in Developing Countries

9.2.2.3 Opportunities

9.2.2.3.1 Scope for Technological Advancements

9.2.2.3.2 Increasing Consumer Awareness About Safety and Quality of Meat & Other Food Products in Emerging Markets

9.2.2.4 Challenges

9.2.2.4.1 Lack of Harmonization of Food Safety Standards

9.2.2.4.2 Gaps in Supply Chain for Meat Certification

9.2.2.4.3 Time Consumed in Certification Procedures

9.3 Competitive Landscape

9.3.1 Overview

9.3.2 Market Share Analysis

9.3.3 Competitive Situation & Trends

9.3.3.1 New Service Launches

9.3.3.2 Expansions & Investments

9.3.3.3 Acquisitions

9.4 Market Analysis

9.4.1 Regional Market Analysis

9.4.2 Meat Speciation Market Analysis, By Species

9.4.3 Meat Speciation Market Analysis, By Technology

10 Pesticide Residue Market (Page No. - 167)

10.1 Market Definition

10.2 Market Overview

10.2.1 Introduction

10.2.2 FDA’s Pesticide Regulatory Monitoring Data, 2013

10.2.3 Market Dynamics

10.2.3.1 Drivers

10.2.3.1.1 Advancements in Testing Technologies

10.2.3.1.2 Global Movement of Organic Revolution

10.2.3.1.3 Implementation of Stringent Food Safety Regulations

10.2.3.1.4 International Trade of Food Materials

10.2.3.2 Restraints

10.2.3.2.1 Lack of Food Control Infrastructure & Resources in Developing Countries

10.2.3.2.2 Lack of Awareness About Safety Regulations Among Food Manufacturers

10.2.3.3 Opportunities

10.2.3.3.1 Expansion Opportunities in Emerging Markets for Pesticide Residue Testing

10.2.3.3.2 Increasing Consumers’ Demand for Food Safety

10.2.3.4 Challenges

10.2.3.4.1 Inappropriate Standard of Sample Collection

10.2.3.4.2 Lack of Standardization of Food Safety Regulations

10.2.4 Introduction

10.3 Competitive Landscape

10.3.1 Overview

10.3.1.1 Pesticide Residue Testing Market Share (Value), By Key Player, 2015

10.3.2 Key Market Strategies

10.3.2.1 Acquisitions

10.3.2.2 Expansions & Investments

10.3.2.3 Innovations, Accreditations, Partnerships, and Collaborations

10.3.2.4 New Service Launches

10.4 Market Analysis

10.4.1 Regional Market Analysis

10.4.2 Pesticide Residue Market Analysis, By Type

10.4.2.1 Hazards of Pesticides

10.4.2.1.1 Impact on Human Life

10.4.2.1.2 Impact on Environment

10.4.3 Pesticide Residue Market Analysis, By Technology

10.4.4 Pesticide Residue Market Analysis, By Food Tested

11 Mycotoxin Testing (Page No. - 192)

11.1 Market Definition

11.2 Market Overview

11.2.1 Introduction

11.2.2 Market Dynamics

11.2.2.1 Drivers

11.2.2.1.1 Implementation of Stringent Regulations Related to Mycotoxin Detection

11.2.2.1.2 International Trade Mandates

11.2.2.1.3 Growing Consumer Awareness

11.2.2.1.4 Consumer Complaints (Food Recalls)

11.2.2.1.5 Humid Atmospheric Conditions Leading to Increase in Mycotoxins

11.2.2.2 Restraints

11.2.2.2.1 Lack of Food Control Systems, Technology, Infrastructure & Resources in Developing Countries

11.2.2.3 Opportunities

11.2.2.3.1 Expansion Opportunities in Emerging Markets for Testing

11.2.2.3.2 Availability of Advanced Technologies Capable of Rapid Testing

11.2.2.4 Challenges

11.2.2.4.1 Unaffordability of Tests and Product Reputation

11.2.2.4.2 Inappropriate Sample Collection & Standardization

11.3 Competitive Landscape

11.3.1 Overview

11.3.2 Mycotoxin Testing Market Share, By Key Player, 2015

11.3.3 Key Market Strategies

11.3.3.1 Expansions & Investment

11.3.3.2 Acquisitions

11.3.3.3 Agreements, Collaborations, Partnerships, and New Technology Launches

11.3.3.4 New Product/Service Launches

11.4 Market Analysis

11.4.1 Regional Market Analysis

11.4.2 Mycotoxin Market Analysis, By Type

12 Allergen Testing (Page No. - 216)

12.1 Market Definition

12.2 Market Overview

12.2.1 Market Dynamics

12.2.1.1 Drivers

12.2.1.1.1 Labeling-Compliance to Drive Allergen Testing

12.2.1.1.1.1 Advisory Labeling

12.2.1.1.2 Growing Allergic Reactions Among Consumers

12.2.1.1.3 Consumer Complaints (Food Recalls)

12.2.1.1.4 Implementation of Stringent Food Safety Regulations

12.2.1.1.4.1 HACCP & GMP Implemented the Most for Allergen Management

12.2.1.1.5 International Trade of Food Materials

12.2.1.2 Restraints

12.2.1.2.1 Lack of Food Control Infrastructure & Resources in Developing Countries

12.2.1.2.2 Lack of Awareness About Labeling Regulations

12.2.1.3 Opportunities

12.2.1.3.1 Technological Advancements in the Testing Industry

12.2.1.3.1.1 Multi-Allergen Screening System

12.2.1.4 Challenges

12.2.1.4.1 Technical Difficulties During Sampling, Testing, and Protein Identification

12.2.1.4.2 Lack of Standardization in Allergen Testing Practices

12.3 Competitive Landscape

12.3.1 Overview

12.3.2 Food Allergen Testing Market Share (Revenue), By Key Player, 2015

12.3.3 Key Market Strategies

12.3.3.1 Expansions & Investments

12.3.3.2 Acquisitions

12.3.3.3 Agreements, Collaborations, Partnerships, and New Technology Launches

12.3.3.4 New Service/Product Launches

12.4 Market Analysis

12.4.1 Regional Market Analysis

12.4.2 Food Allergen Market Analysis, By Source

12.4.3 Food Allergen Market Analysis, By Technology

12.4.4 Food Allergen Testing Market Analysis, By Food Tested

13 Water Testing & Analysis (Page No. - 242)

13.1 Market Definition

13.2 Market Overview

13.2.1 Introduction

13.2.2 Market Dynamics

13.2.2.1 Drivers

13.2.2.1.1 Growing Industrial Applications Spur the Market for Water Testing & Analysis Instruments

13.2.2.1.2 Increasing Government and Private Funding for Tackling Environment Issues

13.2.2.1.3 Technological Integration to Provide End Users With Innovative Products and Improved Capabilities

13.2.2.2 Restraints

13.2.2.2.1 Limited Market Penetration for Water Testing & Analysis Instruments in Non-Industrial Applications

13.2.2.2.2 Reluctance of Municipal Bodies and Civic Societies to Adopt New Technologies

13.2.2.3 Opportunities

13.2.2.3.1 Increasing Awareness About Water Quality

13.2.2.3.2 Rapid Urbanization in Developing Economies

13.2.2.4 Challenges

13.2.2.4.1 High Prices of Water Testing & Analysis Technologies

13.3 Competitive Landscape

13.3.1 Overview

13.3.2 Competitive Situation & Trends

13.3.2.1 New Product & Technology Launches

13.3.2.2 Expansions

13.3.2.3 Acquisitions

13.3.2.4 Agreements, Collaborations & Partnerships

13.4 Market Analysis

13.4.1 Regional Market Analysis

13.4.2 Water Testing & Analysis Market, By Product

13.4.3 Water Testing & Analysis Market, By Product Type

13.4.4 Water Testing & Analysis Market, By Application

14 Bottled Water Testing Market (Page No. - 261)

14.1 Market Definition

14.2 Market Overview

14.2.1 Introduction

14.2.2 Market Dynamics

14.2.2.1 Drivers

14.2.2.1.1 Technological Advancements in Testing Equipment

14.2.2.1.1.1 Solid Phase Extraction (SPE) Tubes

14.2.2.1.1.2 Stable Isotope Labeling and High Resolution Mass Spectrometry

14.2.2.1.1.3 Government Funding for Technological Developments

14.2.2.1.2 Increasing Need for Quality Testing of Water

14.2.2.1.2.1 Emerging Water-Borne Diseases Driving the Testing Market

14.2.2.1.3 Stringent Regulatory Requirement

14.2.2.1.4 Increased Bottled Water Consumption

14.2.2.2 Restraints

14.2.2.2.1 High Cost of Testing Equipment

14.2.2.2.1.1 Adoption of Advanced Testing Methods Proportional to the Price of Sample Testing

14.2.2.3 Opportunities

14.2.2.3.1 Growing Market in Emerging Economies

14.2.2.3.1.1 Testing Laboratories’ Demand for After-Sales Service to Enhance Operational Efficiency

14.2.2.4 Challenges

14.2.2.4.1 High Capital Investment

14.2.2.4.2 Negative Environmental Impact

14.2.2.4.2.1 Increase in Disposable Containers Leads to Pollution, Restricting Growth of the Bottled Water Industry

14.3 Competitive Landscape

14.3.1 Overview

14.3.2 Competitive Situation & Trends

14.3.2.1 New Product Launches

14.3.2.2 Expansions

14.3.2.3 Acquisitions

14.3.2.4 Agreements, Collaborations, and Partnerships

14.4 Market Analysis

14.4.1 Regional Market Analysis

14.4.2 Bottled Water Testing Equipment Market Analysis, By Technology

14.4.3 Bottled Water Testing Equipment Market Analysis, By Component

14.4.4 Bottled Water Testing Equipment Market Analysis By Test Type

15 Company Profiles (Page No. - 280)

(Company at A Glance, Recent Financials, Products & Services, Strategies & Insights, & Recent Developments)*

15.1 Introduction

15.2 SGS S.A.

15.3 Bureau Veritas S.A.

15.4 Intertek Group PLC

15.5 Eurofins Scientific SE

15.6 ALS Limited

15.7 Thermo Fisher Scientific, Inc.

15.8 Merieux Nutrisciences Corporation

15.9 Asurequality Ltd.

15.10 Microbac Laboratories, Inc.

15.11 Romer Labs Diagnostic GmbH

*Details on Company at A Glance, Recent Financials, Products & Services, Strategies & Insights, & Recent Developments Might Not Be Captured in Case of Unlisted Companies.

16 Appendix (Page No. - 325)

16.1 Discussion Guide

16.2 Knowledge Store: Marketsandmarkets’ Subscription Portal

16.3 Introducing RT: Real-Time Market Intelligence

16.4 Recent Developments

16.4.1 Expansions & Investments

16.4.2 Acquitions

16.4.3 New Product Launches

16.4.4 Agreements

16.5 Available Customizations

16.6 Author Details

List of Tables (130 Tables)

Table 1 Growing Middle-Class Population in the Asia-Pacific Region

Table 2 Number of Certification Agencies and Laboratories

Table 3 Number of Certification Agencies and Laboratories in China

Table 4 Mergers & Acquisitions, 2012–January 2017

Table 5 Expansions, 2012–January 2017

Table 6 Joint Ventures, Agreements, Partnerships, Collaborations, & Accreditations, 2012–2017

Table 7 New Service & Technology Launches, 2012–2017

Table 8 Food Safety Testing Market Size, By Region, 2014–2022 (USD Million)

Table 9 Food Safety Testing Market Size, By Contaminant, 2014–2022 (USD Million)

Table 10 Food Safety Testing Market Size, By Technology, 2014–2021 (USD Million)

Table 11 Food Safety Testing Market: Foodborne Pathogens, By Food Source

Table 12 Food Safety Testing Market Size, By Food Tested, 2014–2022 (USD Million)

Table 13 Labeling Requirements in Different Countries

Table 14 Impact of Key Drivers on the GM Food Safety Testing Market

Table 15 Impact of Key Restraints on the GM Food Safety Testing Market

Table 16 Opportunities in the GM Food Safety Testing Market

Table 17 Challenges for the GM Food Safety Testing Market

Table 18 Expansions & Investments, 2012–2017

Table 19 Acquisitions, 2012–2017

Table 20 New Product, Service, and Technology Launches, 2012–2017

Table 21 Agreements, Collaborations, and Partnerships, 2012–2017

Table 22 GM Food Safety Testing Market Size, By Region, 2014–2022 (USD Million)

Table 23 GM Food Safety Testing Market Size, By Trait, 2014–2022 (USD Million)

Table 24 GM Food Safety Testing Market Size, By Technology, 2014–2022 (USD Million)

Table 25 GM Food Safety Testing Market Size, By Crop & Food Tested, 2014–2022 (USD Million)

Table 26 Food Recalls, 2010–2015

Table 27 Allergen Recalls in U.S. (2015)

Table 28 Food Products From U.S. Banned in Other Countries

Table 29 Expansions & Investments, 2016

Table 30 Acquisitions, 2016

Table 31 Agreements, Collaborations, Partnerships & New Technology Launches, 2016

Table 32 New Service Launches, 2015–2016

Table 33 Food Authenticity Testing Market Size, By Region, 2014–2022 (USD Million)

Table 34 Food Authenticity Testing Market Size, By Target Testing, 2014–2022 (USD Million)

Table 35 False Labelling Testing Market Size, By Type, 2014–2022 (USD Million)

Table 36 Food Authenticty Testing Market Size, By Technology, 2014-2022 (USD Million)

Table 37 Number of Certification Agencies and Laboratories in China

Table 38 Acquisitions, 2012–2017

Table 39 Expansions, Investments & Accreditations, 2012–2017

Table 40 Agreements Collaborations, & Partnerships 2012–2017

Table 41 New Service & Technology Launches, 2012–2017

Table 42 Food Pathogen Testing Market Size, By Region, 2014–2022 (USD Million)

Table 43 Food Pathogen Testing Market Size, By Type, 2014–2022 (USD Million)

Table 44 Food Pathogen Testing Market Size, By Food Type, 2014–2022 (USD Million)

Table 45 Food Pathogen Testing Market Size, By Technology, 2013–2020 (USD Million)

Table 46 New Service Launches, 2011–2016

Table 47 Expansions & Investments, 2011–2016

Table 48 Acquisitions, 2011–2016

Table 49 Meat Speciation Testing Market, By Region, 2014-2022 (USD Million)

Table 50 Meat Speciation Testing Market Size, By Species, 2014–2021 (USD Million)

Table 51 Meat Speciation Testing Market Size, By Technology, 2014–2022 (USD Million)

Table 52 Acquisitions, 2011–2016

Table 53 Expansions & Investments, 2011–2016

Table 54 Innovations, Accreditations, Partnerships, and Collaborations, 2011–2016

Table 55 New Service Launches, 2011–2016

Table 56 Pesticide Residue Testing Market Size, By Region, 2014–2022 (USD Million)

Table 57 Pesticide Residue Testing Market Size, By Type, 2014–2022 (USD Million)

Table 58 Pesticide Residue Testing Market Size, By Technology, 2014–2022 (USD Million)

Table 59 Pesticide Residue Testing Market Size, By Food Tested, 2014–2022 (USD Million)

Table 60 Toxic Effects of Mycotoxins

Table 61 Border Rejection Cases Against Mycotoxin Contaminated Foods in Europe

Table 62 Mycotoxin Food Recalls, 2013–2016

Table 63 Optimal Temperature Conditions for Various Mycotoxins

Table 64 Mycotoxin Outbreaks in Developing Countries

Table 65 The Recent Evolution in Detection Methods

Table 66 Expansions & Investments, 2016

Table 67 Acquisitions, 2016

Table 68 Agreements, Collaborations, Partnerships, and New Technology Launches, 2015–2016

Table 69 New Product/Service Launches, 2011–2016

Table 70 Mycotoxin Testing Market, By Region, 2014–2022 (USD Million)

Table 71 Food Mycotoxin Testing Market, By Region, 2014–2022 (USD Million)

Table 72 Feed Mycotoxin Testing Market, By Region, 2014–2022 (USD Million)

Table 73 Mycotoxins: Occurrence, Source, and Health Effects

Table 74 Mycotoxin Testing Market Size, By Type, 2014–2022 (USD Million)

Table 75 Food Mycotoxin Testing Market Size, By Type, 2014–2022 (USD Million)

Table 76 Feed Mycotoxin Testing Market Size, By Type, 2014–2022 (USD Million)

Table 77 Causes of Food-Induced Anaphylaxis in Children, By Country

Table 78 Number of Allergen Recalls, 2010–2015

Table 79 Recent Allergen Recalls in the U.S. in 2015

Table 80 Expansions & Investments, 2011–2016

Table 81 Acquisitions, 2011–2016

Table 82 Agreements, Collaborations, Partnerships, and New Technology Launches, 2011–2016

Table 83 New Services/Product Launches, 2011–2016

Table 84 Food Allergen Testing Market Size, By Region, 2014–2022 (USD Million)

Table 85 Food Allergen Testing Market Size, By Technology, 2014–2022 (USD Million)

Table 86 Food Allergen Testing Market Size, By Food Tested, 2014–2022 (USD Million)

Table 87 Increasing Health Consciousness Among Consumers is Driving the Growth of the Water Testing & Analysis Market

Table 88 Reluctance of Municipal Bodies & Civic Societies to Embrace New Technologies Restraining the Growth of Water Testing & Analysis Market

Table 89 Emerging Markets are Paving New Growth Avenues for Players in the Water Testing & Analysis Market

Table 90 High Prices of Water Testing & Analysis Technologies is A Major Challenge for the Water Testing & Analysis Market

Table 91 New Product & Technology Launches, 2012–January 2017

Table 92 Expansions, 2012-January 2017

Table 93 Acquisitions, 2012-January 2017

Table 94 Agreements, Collaborations & Partnerships, 2012-January 2017

Table 95 Water Testing & Analysis Market Size, By Product, 2014–2022 (USD Million)

Table 96 Water Testing & Analysis Market Size, By Product Type, 2012–2019 (USD Million)

Table 97 Water Testing & Analysis Market Size, By Application, 2014–202 (USD Million)

Table 98 Reported Outbreaks Associated With Bottled Water

Table 99 New Product Launches, 2012–January 2017

Table 100 Expansions, 2012-January 2017

Table 101 Acquisitions, 2012–January 2017

Table 102 Agreements , Collaborations, and Partnerships, 2012–January 2017

Table 103 Bottled Water Testing Equipment Market Size, By Region, 2014–2022 (USD Million)

Table 104 Bottled Water Testing Equipment Market Size, By Technology, 2014–2022 (USD Million)

Table 105 Bottled Water Testing Equipment Market Size, By Component, 2014–2022 (USD Million)

Table 106 Bottled Water Testing Equipment Market Size, By Test Type, 2014–2022 (USD Million)

Table 107 SGS S.A.: Services Offered

Table 108 SGS S.A.: Recent Developments

Table 109 Bureau Veritas S.A.: Services Offered

Table 110 Bureau Veritas S.A.: Recent Developments

Table 111 Intertek Group PLC: Services Offered

Table 112 Intertek Group PLC.: Recent Developments

Table 113 Eurofins Scientific: Services Offered

Table 114 Eurofins Scientific: Recent Developments

Table 115 ALS Limited: Services Offered

Table 116 ALS Limited: Recent Developments

Table 117 Thermo Fisher Scientific, Inc.: Products Offered

Table 118 Thermo Fisher Scientific, Inc.: Recent Developments

Table 119 Merieux Nutrisciences Corporation: Services Offered

Table 120 Merieux Nutrisciences Corporation: Recent Developments

Table 121 Asurequality Limited : Services Offered

Table 122 Asurequality Limited: Recent Developments

Table 123 Microbac Laboratories, Inc.: Services Offered

Table 124 Microbac Laboratories, Inc.: Recent Developments

Table 125 Romer Labs Diagnostic GmbH: Services/Products Offered

Table 126 Romer Labs Diagnostic GmbH: Recent Developments

Table 127 Expansions & Investments, 2012–January 2017

Table 128 Acquisitions, 2012–January 2017

Table 129 New Product, Technology & Service Launches, 2012–January 2017

Table 130 Agreements, Collaborations & Partnerships, 2012–January 2017

List of Figures (117 Figures)

Figure 1 Food Safety Testing & Technologies Market: Research Design

Figure 2 Global Population, 2011-2015

Figure 3 TBT-Specific Trade Concerns From 2010 to 2014

Figure 4 Global Food Diagnostics Market Size, 2012-2016 (USD Million)

Figure 5 Market Size Estimation Methodology: Bottom-Up Approach

Figure 6 Market Size Estimation Methodology: Top-Down Approach

Figure 7 Data Triangulation Methodology

Figure 8 Food Safety Testing Market Snapshot, By Sub Markets

Figure 9 Food Safety Testing Market Size (Value), By Region, 2016–2022

Figure 10 GM Food Safety Testing Market Size (Value), By Region, 2016–2022

Figure 11 Food Pathogen Safety Testing Market Size (Value), By Region, 2016–2022

Figure 12 Meat Speciation Testing Market Size (Value), By Region, 2016–2022

Figure 13 Food Authenticity Testing Market Size (Value), By Region, 2016–2022

Figure 14 Water Safety Testing Market Snapshot, By Sub Markets, 2016 vs 2022

Figure 15 Food Safety Testing Market Share (Value), By Region, 2015

Figure 16 Increasing Number of Foodborne Illnesses Worldwide to Drive the Growth of the Food Safety Testing Market

Figure 17 China to Be the Fastest Growing Food Safety Testing Market From 2016 to 2022

Figure 18 Market Dynamics: Food Safety Testing

Figure 19 Rate of Contamination Increase, By Pathogen

Figure 20 Mergers & Acquisitions: Leading Approaches of Key Companies

Figure 21 Mergers & Acquisitions Fueled Growth, 2012–2017

Figure 22 Mergers & Acquisitions: the Key Strategy, 2012- January 2017

Figure 23 U.S. Held the Largest Market Share in Food Safety Testing Market, 2015

Figure 24 Key Factors Responsible for Food Contamination & Foodborne Illnesses, 2013–2014

Figure 25 Meat & Poultry Dominated the Food Safety Testing Market, 2015

Figure 26 U.S.: Food Commodities Responsible for Illnesses, 2000–2014

Figure 27 High Usage of GMO in Processed Foods Drives the GM Food Safety Testing Market

Figure 28 Expansions & Investments Were Preferred By Key GM Food Safety Testing Companies in the Last Five Years

Figure 29 Strengthening Market Presence Through Expansions & Investments, 2012–2017

Figure 30 Expansion & Investments: the Key Strategies, 2012–2017

Figure 31 Research Studies Trend in Food Authenticity

Figure 32 Market Dynamics: Food Authenticity Testing Market

Figure 33 Survey Results on Labeling Requirement of Consumers to Minimise Unintentional Contamination & Food Frauds

Figure 34 Major Incidents of Economically Motivated Adulterations (EMA) From 1980 to 2013

Figure 35 Types of Food Fraud Cases Across World

Figure 36 Acquisitions, Expansions & Investments: Leading Approach of Key Companies

Figure 37 Food Authenticity Testing Market Developments, By Growth Strategy, 2011–2016

Figure 38 Food Authenticity Testing Market Growth Strategies, By Company, 2011–2016

Figure 39 U.S. Held the Largest Share in the Food Authenticity Testing Market, 2015

Figure 40 PCR-Based Technology is Projected to Fastest Growing in Food Authenticty Testing Market, 2014-2022 (USD Million)

Figure 41 Market Dynamics: Food Pathogen Testing Market

Figure 42 Food Safety: Top Concerns of Consumers

Figure 43 U.S. Food Supply: Consumer Perception, 2007–2010

Figure 44 Acquisitions Were Preferred By Key Food Pathogen Testing Companies in the Last Five Years

Figure 45 Acquisitions Fueled Growth, 2012–2017

Figure 46 Acquisition: the Key Strategy, 2012- 2017

Figure 47 Geographic Snapshot: New Hotspots Emerging in Asia-Pacific, (2016–2022)

Figure 48 Stages of Food Contamination

Figure 49 Food Pathogen Testing Market Share, By Technology, 2015 (USD Million)

Figure 50 Leading EMA Food Fraud Incidents, 2013

Figure 51 Leading EMA Food Fraud Incidents, By Region, 2013

Figure 52 Market Dynamics: Meat Speciation Testing

Figure 53 Key Companies Preferred New Service Launches and Expansions & Investments Over the Last Five Years

Figure 54 Expanding Revenue Base Through New Service Launches, 2013–2015

Figure 55 New Service Launches: the Key Strategy, 2011–2016

Figure 56 U.S. Accounted for the Largest Share in the Meat Speciation Testing Market in 2015

Figure 57 Meat Speciation Testing Market Size, By Species, 2016–2022 (USD Million)

Figure 58 Meat Speciation Testing Market Share, By Technology, 2015

Figure 59 FDA’s Pesticide Regulatory Monitoring Data, 2013

Figure 60 Market Dynamics: Pesticide Residue Testing

Figure 61 Chemical Products, Pesticides & Toxic Substances are A Major Concern for European Consumers

Figure 62 U.S.: Food Commodities Responsible for Illnesses, 2000–2014

Figure 63 Acquistions and Expansions & Investments: Leading Approach of Key Companies

Figure 64 Top Five Players Led the Pesticide Residue Testing Market, 2015

Figure 65 Pesticide Residue Testing Market Developments, By Growth Strategy, 2011–2016

Figure 66 Share of Developments in Pesticide Residue Testing Market, By Company, 2011–2016

Figure 67 Acquisitions: the Key Growth Strategy, 2011–2016

Figure 68 U.S. Accounted for the Largest Share in the Pesticide Residue Testing Market in 2015

Figure 69 Herbicides Projected to Be the Fastest-Growing Segment in the Pesticide Residue Testing Market During the Forecast Period

Figure 70 LC-MS/GC-MS is Projected to Be Fastest Growing Segment in the Pesticide Residue Testing Market During the Forecast Period

Figure 71 Processed Food Dominated the Pesticide Residue Testing Market in 2015

Figure 72 Market Dynamics: Mycotoxin Testing Market

Figure 73 Acquisitions, Expansions & Investments: Leading Approach of Key Companies

Figure 74 Intertek Group PLC the Food Mycotoxin Testing Market, 2015

Figure 75 Mycotoxin Testing Market Developments, By Growth Strategy, 2011–2016

Figure 76 Mycotoxin Testing Market Growth Strategies, By Company, 2011–2016

Figure 77 Competitive Situation and Trends

Figure 78 U.S. Held the Largest Market Share in Mycotoxin Testing Market, 2015

Figure 79 Key Areas of Consideration for Allergen Management in A Supply Chain

Figure 80 Market Dynamics: Food Allergen Testing Market

Figure 81 Proper Labeling to Minimize the Allergen Cross-Contact & Unintentional Contamination

Figure 82 ‘May Contain’ in Advisory Labeling Was Preferred the Most By Consumers

Figure 83 Food Allergy Prevalence in 2013 Among Children of All Ages (0–18 Years)

Figure 84 HACCP & GMP Implemented the Most for Allergen Management

Figure 85 Acquisitions, Expansions, and Investments: Leading Approach of Key Companies

Figure 86 TUV SUD PSB PTE. Ltd. Led the Food Allergen Testing Market, 2015

Figure 87 Food Allergen Testing Market Developments, By Growth Strategy, 2011–2016

Figure 88 Food Allergen Testing Market Share (Developments), By Company, 2011–2016

Figure 89 Competitive Situations & Trends

Figure 90 The U.S. Held the Largest Share in the Food Allergen Testing Market, 2015

Figure 91 Food Allergen Testing Market Size, By Source, 2016 vs 2022 (USD Million)

Figure 92 Advancements in Immunoassay (Elisa) Technology Drives the Food Allergen Testing Market Growth

Figure 93 Food Allergen Testing Market Share, By Food Tested

Figure 94 Rapid Urbanization Provides an Opportunity for Market Growth

Figure 95 New Product & Technology Launches Were Preferred By Key Water Testing & Analysis Companies in the Last Five Years

Figure 96 New Product & Technology Launches Fueled Growth, 2012–January 2017

Figure 97 Acquisition: the Key Strategy, 2012-January 2017

Figure 98 Geographical Snapshot (2016-2022): Asia-Pacific Emerging as A New Hot Spot for Water Testing & Analysis

Figure 99 Stringent Regulatory Environment to Drive Growth of Bottled Water Testing Equipment

Figure 100 Global Bottled Water Testing Market, (2009-2014)

Figure 101 New Product Launches: Leading Strategy of Key Companies

Figure 102 Expanding Revenue Base Through New Product Launches, 2012–January 2017

Figure 103 New Product Launches: the Key Strategy, 2012–January 2017

Figure 104 Asia-Pacific to Witness the Fastest Growth Between 2016 & 2022

Figure 105 Geographic Revenue Mix of Top Five Market Players

Figure 106 SGS SA: Company Snapshot

Figure 107 SGS S.A.: SWOT Analysis

Figure 108 Bureau Veritas S.A.: Company Snapshot

Figure 109 Bureau Veritas SA: SWOT Analysis

Figure 110 Intertek Group PLC: Business Overview

Figure 111 Intertek Group PLC: SWOT Analysis

Figure 112 Eurofins Scientific SE: Company Snapshot

Figure 113 Eurofins Scientific SE: SWOT Analysis

Figure 114 ALS Limited: Company Snapshot

Figure 115 ALS Limited: SWOT Analysis

Figure 116 Thermo Fisher Scientific, Inc.: Company Snapshot

Figure 117 Asurequality Limited: Company Snapshot

Growth opportunities and latent adjacency in Top 10 Food Safety Testing and Technologies Trends